What Is the Other Than Products-Completed Operations Aggregate Limit?

If you are a business owner or contractor reviewing a Certificate of Insurance (COI) or a Commercial General Liability (CGL) policy declarations page, the terminology can feel deliberately confusing. You might see a massive dollar amount listed next to the phrase "Other Than Products-Completed Operations" and wonder exactly what risks that money is meant to cover.

Understanding this specific limit is critical. It serves as the primary financial shield for your day-to-day operations. Misinterpreting how this limit functions—or how it interacts with the rest of your policy—can leave your business exposed to devastating out-of-pocket legal costs.

What Does "Other Than Products-Completed Operations" Actually Mean?

To understand this phrase, you have to understand how insurance policies are constructed. The insurance industry frequently relies on standardized forms created by the Insurance Services Office (ISO), specifically the widely used Form CG 00 01. These forms often define coverage not by listing every single thing that is included, but by establishing a broad baseline and then explicitly stating what is excluded.

This is known as a subtractive definition. The "Other Than" phrasing exists because this limit acts as a catch-all. Instead of trying to list every conceivable accident that could happen while you are running your business, the policy states that this aggregate limit covers everything except claims related to your finished products or completed operations.

According to Aligned Insurance, on most standard COIs, this line item is entirely synonymous with the General Aggregate Limit. It is the annual cap—the maximum "bucket" of funds available for the entire 12-month policy period to pay for settlements, judgments, and often legal defense costs related to general operational hazards.

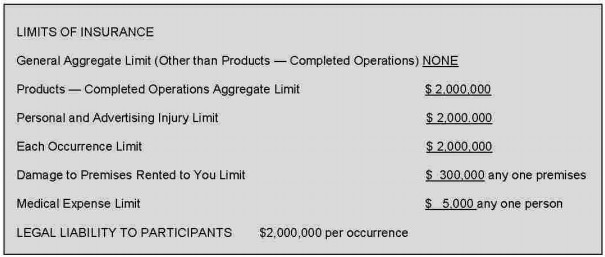

Image source: Sadler Sports & Recreation Insurance

How the Two-Bucket Aggregate System Works

A standard Commercial General Liability policy is structured around a "two-bucket" system. These two buckets of money are distinct and do not spill into each other. This separation ensures that a massive lawsuit regarding a defective product doesn't completely drain the funds you need to cover a slip-and-fall accident in your office lobby.

The two buckets are:

- Bucket A: The General Aggregate (The "Other Than" limit). This covers your premises, your ongoing operations, and general business liabilities.

- Bucket B: The Products-Completed Operations (PCO) Aggregate. This covers claims arising from goods you have sold or work you have finished and walked away from.

It is crucial to understand how these aggregate limits interact with your Per Occurrence limit. The Per Occurrence limit acts as a valve on the bucket. If you have a $1,000,000 Per Occurrence limit and a $2,000,000 General Aggregate limit, a single severe accident can only drain a maximum of $1,000,000 from the bucket. However, as the International Risk Management Institute (IRMI) notes, a single claim payment reduces the Per Occurrence limit and the applicable Aggregate limit simultaneously.

If you suffer two separate $1,000,000 claims in the same year under the General Aggregate, your $2,000,000 bucket is now empty. You are effectively uninsured for any further general liability claims for the remainder of the policy term.

What Is Covered Under the General Aggregate Limit?

Because the "Other Than" limit is a catch-all, it encompasses several distinct categories of coverage within your CGL policy. Specifically, it applies to claims falling under Coverage A, B, and C (provided they do not involve finished products or completed work).

-

Coverage A: Bodily Injury and Property Damage (Ongoing Operations)

This is the core of your daily liability protection. It covers accidents that happen on your business premises (like a customer slipping on a wet floor) or damage caused while your crew is actively working on a job site. If your employee accidentally drives a forklift through a client's wall while delivering materials, the resulting property damage claim draws from this limit. -

Coverage B: Personal and Advertising Injury

This covers non-physical injuries to third parties. Common examples include libel, slander, copyright infringement in your marketing materials, or false arrest. If you publish a social media post that damages a competitor's reputation and they sue you, the defense and settlement costs are pulled from the General Aggregate. -

Coverage C: Medical Payments

This is a "no-fault" coverage designed to handle minor injuries quickly without the need for a lawsuit. If a visitor trips in your store and needs stitches, Coverage C can pay their immediate medical bills. These payments also reduce your General Aggregate limit for the year.

One of the most critical aspects of aggregate limits is how they affect your legal defense. Under standard ISO forms, the insurance company's "duty to defend" you in court ends the moment the aggregate limit is exhausted by the payment of judgments or settlements. If your bucket is empty, you are not only responsible for paying future damages out of pocket, but you must also hire and pay for your own legal counsel.

General Aggregate vs. Products-Completed Operations Aggregate

To fully grasp the "Other Than" limit, you must understand exactly what it is being contrasted against. The Products-Completed Operations (PCO) aggregate handles the long-tail risks of running a business. According to The Hartford, PCO coverage is triggered when a product has left your physical possession or when a service/construction project has been finished and put to its intended use.

| Feature | General Aggregate ("Other Than") | Products-Completed Operations (PCO) |

|---|---|---|

| Coverage Trigger | During active work or on business premises. | After work is finished or product is sold/relinquished. |

| Common Example | A customer trips over an extension cord in your shop. | A deck you built collapses six months later, injuring the homeowner. |

| Limit Reset | Resets at the start of each new policy term. | Resets at the start of each new policy term. |

| Primary Risk Profile | High frequency, immediate incidents. | Low frequency, delayed "long-tail" incidents. |

The "Impaired Property" Distinction

A common point of confusion for contractors is assuming that these aggregate limits act as a warranty for their work. They do not. Neither bucket typically pays to fix your own faulty workmanship. They only pay for the bodily injury or property damage that your faulty work causes to others. If you install a roof poorly and it leaks, the policy will not pay to replace the roof (your work), but the PCO aggregate may cover the cost of the ruined hardwood floors inside the house (resulting damage).

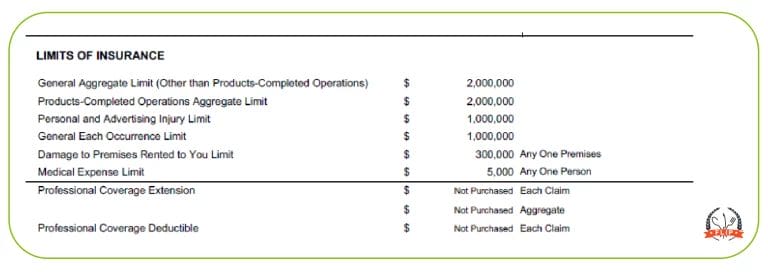

Image source: Food Liability Insurance Program (FLIP)

Real-World Examples of Claims in Each Bucket

To clarify how claims are categorized, let's look at how different scenarios draw from different aggregate limits.

The Dropped Hammer

A roofing contractor is actively working on a house. A worker drops a hammer off the edge of the roof, striking a pedestrian walking on the sidewalk below. Because the contractor is still on-site and the operations are ongoing, the resulting bodily injury claim is paid out of the General Aggregate ("Other Than") limit.

The Exploding Widget

A manufacturer produces and sells a batch of toasters. Six months later, a defect causes one of the toasters to catch fire in a customer's kitchen, causing severe property damage. Because the product had left the manufacturer's control and was put to its intended use, this claim draws from the Products-Completed Operations aggregate.

The Libel Suit

A local bakery owner posts a disparaging and factually incorrect comment about a rival bakery's health standards on social media. The rival sues for defamation and loss of income. This falls under Coverage B (Personal and Advertising Injury) and is paid out of the General Aggregate limit.

The Burst Pipe Transition

If a plumber is tightening a pipe and it bursts, causing water damage, it hits the General Aggregate. However, if the plumber finishes the job, goes home, and the pipe bursts two weeks later due to a faulty seal, the resulting water damage claim transitions to the PCO Aggregate.

Common Pitfalls and Coverage Gaps to Avoid

Managing your CGL policy requires careful attention to dates, endorsements, and specific policy language. Several technical nuances can lead to severe coverage gaps if misunderstood.

The Policy Extension Trap

Businesses sometimes request to extend their 12-month policy by a few months to align their insurance renewal date with their fiscal year. This can be a dangerous maneuver. As highlighted by risk management experts, extending a policy period usually does not increase the aggregate limit. If you extend a 12-month policy to 15 months, your original aggregate limit must now stretch to cover an additional three months of exposure, effectively diluting your protection.

The "Tail" Misconception

Many contractors believe that because they carried PCO coverage during the year they built a structure, they are covered forever for that specific job. This is a misunderstanding of how "occurrence" policies work. For a claim to be covered, the injury or damage (the occurrence) must happen during the active policy period. If you cancel your policy and a deck you built three years ago collapses the next day, you have no coverage, because the injury occurred after the policy was canceled.

The Exclusion Endorsement (CG 21 04)

When reviewing your policy, you must check for specific exclusion endorsements. Discussions among tradespeople on platforms like the Practical Machinist forum reveal a common industry friction point: many low-cost liability policies specifically exclude PCO coverage entirely to keep premiums down.

While standard ISO forms bundle both aggregates together, insurers frequently attach endorsement CG 21 04 (Exclusion - Products-Completed Operations Hazard) for high-risk trades or manufacturing operations. If this endorsement is on your policy, your "Other Than" limit is your only limit, and you have zero coverage for anything that happens after you finish a job or sell a product. Note that data on how often this occurs varies; some sources suggest it is standard practice for high-risk manufacturing, while others note it is rarely applied to standard retail businesses. Always verify your specific declarations page.

Why Do Clients Require Specific Aggregate Limits?

If you are a subcontractor or a vendor, you have likely received a contract demanding specific limits for both the General Aggregate and the PCO Aggregate—often $2,000,000 or higher. There are specific legal and financial reasons for these requirements.

First, it is a matter of contractual compliance and risk transfer. General contractors and large corporate clients want to ensure that if your work causes a massive loss, your insurance bucket is deep enough to pay for it before their own insurance has to step in. A $2M aggregate is widely regarded as the baseline standard for commercial contracts because it provides a sufficient buffer against multi-party lawsuits or severe property damage.

Second, these limits are often tied to Umbrella or Excess Liability policies. An umbrella policy will not "drop down" to cover a claim unless the underlying primary policy meets specific minimum limits. If a vendor requires you to carry a $5M umbrella policy, the insurer writing that umbrella will almost certainly demand that your underlying General Aggregate is at least $2M.

Image source: LandesBlosch

Frequently Asked Questions

- Does the General Aggregate include products and completed operations?

- No. The General Aggregate and the Products-Completed Operations Aggregate are two separate limits (or "buckets") of money. Claims are categorized into one or the other based on whether the work was ongoing or finished at the time the injury or damage occurred.

- What happens if I hit my aggregate limit mid-year?

- If your aggregate limit is exhausted by paid claims and settlements, you are essentially uninsured for that specific category of risk for the remainder of the policy term. Furthermore, the insurance company's duty to pay for your legal defense also ends, leaving you responsible for all future legal costs.

- Is "Other Than Products" the same as "Premises-Operations"?

- In most practical contexts, yes. "Premises-Operations" is an older, more descriptive term for the types of risks covered under the General Aggregate. The modern ISO terminology uses the subtractive "Other Than Products-Completed Operations" phrasing, but they refer to the same bucket of coverage.

- Does the limit reset if I change insurance companies?

- Yes. Aggregate limits apply to a specific policy period (usually 12 months). If you switch to a new insurance carrier and start a new policy, you begin with fresh, full aggregate limits for that new term.

- Why is my PCO aggregate lower than my General aggregate?

- This is common in trades where the long-term risk of a product failing is deemed higher or more unpredictable than the daily operational risk. Insurers may offer a $2M General Aggregate but restrict the PCO Aggregate to $1M to limit their exposure to long-tail claims that could surface years later.

- Does this limit cover injuries to my employees?

- No. Commercial General Liability policies strictly exclude injuries to your own employees. Employee injuries must be covered by a separate Workers' Compensation policy.

Final Thoughts

The "Other Than Products-Completed Operations" aggregate is the financial foundation of your daily business liability protection. By understanding that this limit is defined by what it excludes, you can better navigate your insurance documents and ensure you are meeting client contract requirements.

- Identify the "Other Than" limit on your COI as your primary General Aggregate for daily operations and premises liability.

- Verify that your policy does not contain an endorsement (like CG 21 04) that entirely excludes your Products-Completed Operations coverage.

- Monitor your total claims throughout the year to ensure you are not nearing the exhaustion point, which would terminate your legal defense coverage.

- Recognize the difference between ongoing work (General Aggregate) and finished work (PCO Aggregate) to understand how future claims will be categorized.

- Avoid extending your policy period beyond 12 months without explicitly negotiating a proportional increase in your aggregate limits.